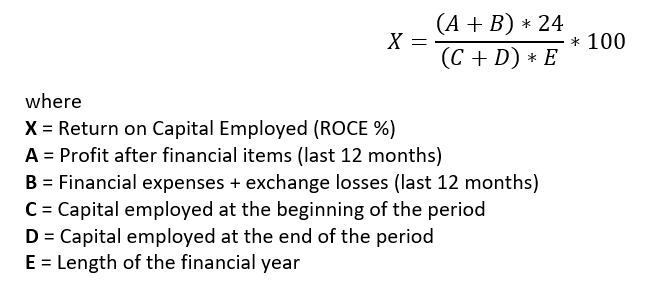

The return on capital indicators are part of the standard key‑ratio calculation, which can be found on the Reports tab by selecting Ratios. The following formulas are used to calculate these indicators:

Return on capital employed (ROCE-%)

Return on invested capital describes the relationship between the profit generated from core business operations and the capital resources committed to achieving that profit.

The coefficient 24 in the numerator results from taking into account the length of the financial year and the fact that the denominator contains the sum of the capital employed at the beginning and at the end of the period. Capital employed is calculated as the average of the beginning‑ and end‑of‑period values.

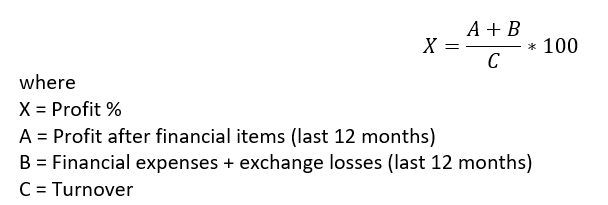

Return on investment (ROI)

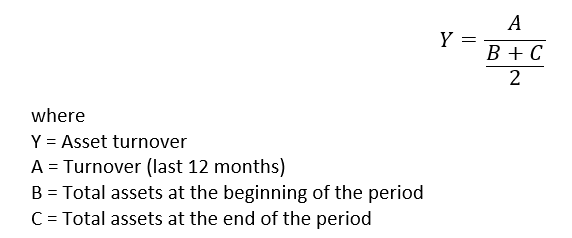

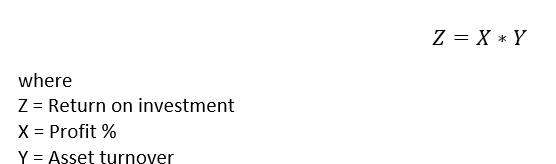

The return on investment can be used to monitor a company’s internal profitability, and it is particularly suitable for profit‑center organizations. The return on investment is obtained as the product of the profit margin and the capital turnover rate.

Profit %:

Asset turnover:

ROI, Return On Investment:

Profitability expressed as return on investment can be improved by increasing the profit margin and/or the capital turnover. However, these two components often conflict with each other; for example, increasing the profit margin may lead to a decrease in the turnover rate